On 29 November, CDSB and CDP published the report ‘First Steps’ which examined corporate climate and environmental disclosure in the first year of reporting under the EU Non-Financial Reporting Directive. In this summary, we look at some of the findings and the next steps we recommend.

Since its inception, CDSB has been vocal in advocating the need for mandatory and mainstream reporting of climate and environmental information. When it was first released, the Non-Financial Reporting Directive was welcomed by CDSB as a momentous step in the trajectory towards achieving EU-wide standardisation of non-financial reporting. Recognising that natural capital and financial capital are equally vital for an understanding of corporate performance will be essential in securing a more sustainable and resilient financial system. European countries are pioneering the field in providing the foundations for achieving this goal and the Directive forms a critical part of this process.

Our research in the recently published report 'First Steps' comes at a pivotal moment as the Commission is undertaking a review of the corporate reporting framework in Europe to assess if it is fit for function. The findings are expected in Summer 2019. CDSB’s clear purpose when compiling the report was to provide the European Commission, Parliament and Council with the informative evidence necessary to understand the effectiveness of the Directive in shaping the environmental and climate reporting landscape.

What we found

This review assembles evidence of reporting practices by companies on environmental matters in the first year of reporting under the EU Non-Financial Reporting Directive (NFRD). We focused on the management reports of a core sample of 80 companies, assessing their annual reports to determine whether they have sufficiently disclosed information relating to environmental matters under the five ‘Content Categories’ of the NFRD. The report provides essential insight into what information companies are currently reporting, and whether their disclosures are successful in the implementation of the 11 recommendations of the G20 Task Force on Climate-related Financial Disclosures (TCFD). Our research offers the first comprehensive review of the Directive and its use by companies.

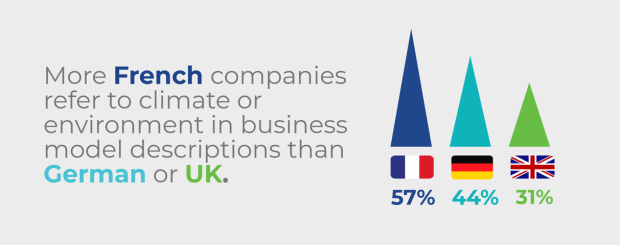

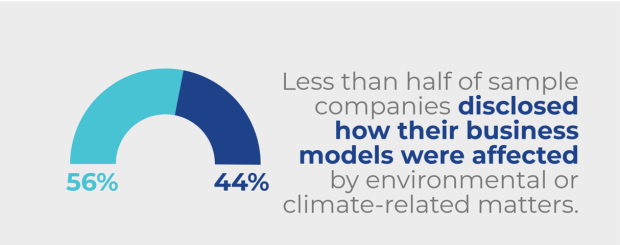

The findings showed several differences in disclosures of environmental and climate-related information across the 'Content Categories' of the NFRD. Below is a selection of the key findings from the report:

In addition, the findings indicate that the NFRD could be further enhanced by becoming more closely aligned to the voluntary TCFD recommendations. There is considerable overlap between the TCFD and the NFRD: the four core elements in the TCFD: governance, strategy, risk management and metrics already feature in the 'Content Categories' of the NFRD.

Next steps

We recommend that for the NFRD to continue to be meet its objective "to increase EU companies’ transparency and performance on environmental and social matters and, therefore, to contribute effectively to long-term economic growth and employment”, it would benefit from promoting the concept of forward-looking information. Forward-looking disclosures would encourage investors to identify both opportunities and risks to business arising from natural capital and climate change.

The TCFD promotes scenario analysis as a useful tool in assessing both negative and positive climate-related impacts on a company. At present, the Directive omits any mention of scenario analysis. By incorporating the recommended disclosures of the TCFD, including scenario analysis, the Directive would deliver the quality of forward-looking climate-related financial information that investors require for effective and informed decision making.

The NFRD represents a strong first step to set a baseline for Europe, but as our report shows, the Directive could benefit further from clarification and embracing closer alignment with the TCFD's recommended disclosures. We conclude our research with 7 clear recommendations, which we believe would greatly improve both the uptake and the effectiveness of reporting.

To read the full report visit cdsb.net/NFRreview.