|

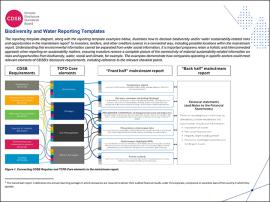

Biodiversity and water reporting templates

CDSB has created a reporting template diagram and examples to illustrate how to disclose biodiversity and/or water sustainability-related risks and opportunities in the mainstream report to investors, lenders, and other creditors (users) in a connected way, including possible locations within the mainstream report. |

|||

|

Mastering through mainstreaming: TCFD Disclosures in the mainstream financial report | |||

|

Net Zero: walking the talk

Practical steps for a connected Net Zero and TCFD-aligned mainstream financial report This paper aims to help companies quickly move beyond commitments to comprehensive reporting on their action plans and progress towards net zero. Businesses can do so via the following routes: getting to grips with the science behind net zero, and guidance on how net zero can be integrated and form part of the comprehensive net zero reporting in the mainstream financial report, including insights on how to connect with TCFD principles of transition plans, scenario analysis and financial reporting. |

|||

|

European policy briefing: From theory to practice, the role of supervisors in improving corporate reporting in the EU

This paper aims to discuss the critical role supervision plays to strengthen corporate sustainability disclosures and prevent greenwashing. It also provides resources and practical recommendations to national supervisors. |

|||

|

Accounting for climate: summary for EU policymakers

This summary for EU policymakers provides an overview of the information presented in CDSB's 'Accounting for climate’ report, published in December 2020. Accounting for climate was produced to support report preparers in integrating climate-related matters into financial statements. |

|||

|

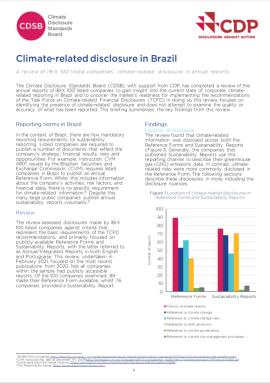

Climate-related disclosure in Brazil This paper provides a review of IBrX 100 listed companies' climate-related disclosure in annual reports with insights into the current state of corporate climate-related reporting in Brazil and market's readiness for implementing the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). Click here to access this and more resources translated to Portuguese language. |

|||

|

What, Why & How: Decision-useful climate-related information for investors This paper seeks to highlight the specific climate-related information, in line with the Task Force on Climate-related Financial Disclosures (TCFD) recommendations, that investors consider to be useful when it comes to their own decision-making process. |

|||

|

Water-related disclosure briefing: The state of EU environmental disclosure in 2020 This briefing will provide an overview of the findings of "The State of EU Environmental disclosures in 2020" review with respect water-related disclosures and provides recommendations for companies, policymakers and regulators. It complements two further topic briefings on climate-related and on biodiversity, deforestation and forest degradation-related disclosure. |

|||

|

Climate and TCFD disclosure briefing: The state of EU environmental disclosure in 2020

This briefing provides an overview of the findings of "The State of EU Environmental disclosures in 2020" review with respect to TCFD and climaterelated disclosures and provides recommendations for companies, policymakers and regulators. It complements two further topic briefings on water-related and on biodiversity and deforestation and forest degradation-related disclosure. |

|||

|

Briefing on biodiversity, deforestation and forest degradation disclosure in the EU

This briefing provides an overview of the findings of "The State of EU Environmental disclosures in 2020" review with respect to biodiversity, deforestation, and forest degradation disclosures and provides recommendations for companies, policymakers and regulators. It complements two further topic briefings on climate-related and on water-related disclosure. |

|||

|

Briefing on country-specific disclosures under the EU Non-Financial Reporting Directive These briefings provide an overview of country-specific findings of "The State of EU Environmental disclosures in 2020" report. Country-specific disclosure features are identified and a set of recommendations for policymakers provided. |

|||

|

Briefing: environmental and climate-related disclosure under the EU Non-Financial Reporting Directive In May 2020 CDSB published the "Falling short" report. In this report we reviewed the environmental and climate-related disclosures of Europe’s 50 largest listed companies under the EU Non-Financial Reporting Directive (NFRD), in 2019. The briefings below summarise the findings and recommendations of the report with respect to specific topics or select EU countries. |

|||

|

|

Implications of climate science for financial markets Synthesis of the UN Intergovernmental Panel on Climate Change's Global Warming of 1.5°C special report for financial policymakers. |

|||

|

Roadmap for adopting the TCFD recommendations Under France’s presidency there is the opportunity and urgent need for G7 countries to take action to strengthen climate-related financial disclosures. This roadmap is designed for consideration by the French G7 Presidency and the G7 Ministers of Finance and Environment. |

|||

|

This short guide by CDSB Technical Working Group member, Dr Jane Thostrup Jagd proposes a two-stage process to create key outputs from scenario analysis to be disclosed within mainstream reports that help investors in comparing and aggregating company data to portfolio-level data. |

|||

|

Uncharted waters: how can companies use financial accounting standards to deliver on the TCFD recommendations?This paper focuses on IFRS 7, 9, 15, 17 and IAS 36 and 37, exploring some of the main points applied to traditional financial instruments and how they could help organizations report information about climate-related risks and opportunities in their mainstream report. |

|||

|

Position paper: Materiality and climate-related financial disclosuresIn this paper, CDSB looks at what the TCFD and other mainstream reporting requirements says about the application of materiality to climate-related financial disclosures, trying to understand the main challenges and potential solutions for an effective materiality judgement process. |

|||

|

Position paper on relevance & materiality, organisational boundaries and assuranceThe purpose of this document is to explain the positions that CDSB has adopted in relation to three key themes in the CDSB Framework for Reporting Environmental Information and Natural Capital (the “CDSB Framework”). These are: relevance and materiality; organisational boundary setting; and assurance. |

|||

|

Considerations for reporting and disclosure in a carbon-constrained worldThis paper by Carbon Tracker and CDSB is designed to assist the Task Force on Climate-related Financial Disclosures members in assessing the ‘carbon bubble’ concept and ‘stranded asset’ risks inherent in the business-as-usual strategies of many fossil fuel companies. |

|||

|

Proposals for reporting on Carbon Asset Stranding RisksThis discussion paper addressing CASRs in mainstream reports proposes both amendments to existing legislation and new requirements to reporting laws, standards and practices. The proposed changes are designed to encourage companies to account for and report in a way that enables investors and other users of mainstream corporate reports to identify, assess and respond to CASRs. |

|||

|

Proposals for boundary setting in mainstream reports: discussion paper on organisational boundary setting by groups of companies or non-financial reporting purposesThis discussion paper explores the issue of organisations boundary setting for non-financial reporting purposes and offers some answers to the challenges identified. |